Source: ABC

Unless you’ve been sleeping under a rock, the entire world is talking and writing about Greece, and it is not in relation to Flight Centre’s (FLT) latest holiday package deal.

Seriously, let’s dissect where we are at with Greece and look for where the opportunities are.

At Peak Asset Management, we believe divergence to be the key theme going forward. That is, interest rates are expected to rise in the U.S. due to its strong economy against interest rate cuts in Australia, China and India and quantitative easing across Europe as these latter economies struggle. No matter how hard Greece tries, it is not going to crack this theme with its soap opera.

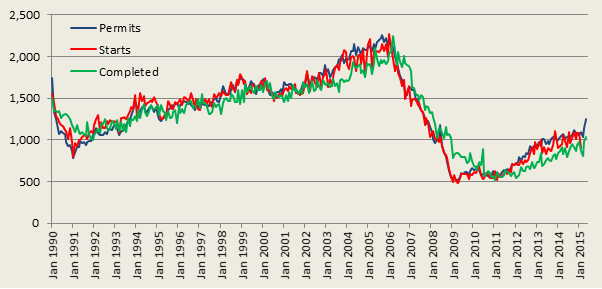

Even within this macro divergence theme, there is another divergence amid the US outlook. A micro-divergence if you will. Strong data continues to come out of the U.S. but their GDP numbers are not looking great. U.S. GDP was revised from a positive 0.2% to -0.7% for the first quarter of 2015. Compare this to 2.20% in the last quarter in FY14 and it is still lower than the long term average of 3.26%. Although building starts fell for the month of May, the overall housing market still looks healthy with an upward trend.

At Peak, we don’t see any reason to decrease our exposure to the U.S. unless something drastic like a Fed hike happens. The Fed has kept interest rates at zero for the last 7 years since the financial crisis in 2008. We do not believe interest rates will be hiked any time soon. We see the latter end of the year as the likeliest time for rate hikes and September at the earliest. But once it does happen, a lot of things will change along with our core beliefs.

U.S. Housing Market

Data Source: ABS

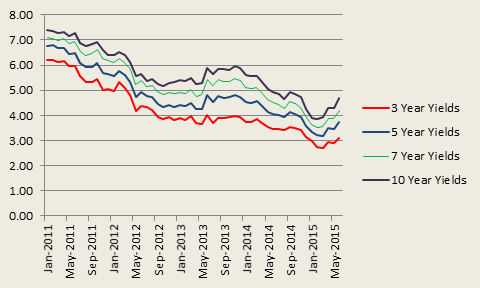

Coming back home, Greece is having an effect on the markets despite Australia’s lack of direct exposure to Greece. Even the risk of a contagion effect is very low. However, there is an overall sentiment of rising risk which is being priced in the corporate bond market with yields creeping upwards of around 20 – 30 basis points in the last 2 months.

Australian Yield Curves

Data Source: RBA

Last month, the AFR had an article discussing how our market stands compared to the world. Goldman Sach’s Equity strategist, Matthew Ross, considers our local sharemarket to be cheap at current levels. The local sharemarket is trading at a discount of 9% compared to the global sharemarkets on a forward price-earnings ratio basis. Ross further points out that on a price to book ratio basis the local sharemarket is at its largest discount in 10 years at 16% to the MSCI World index.

MSCI Aust. vs World Relative P/E

Source: AFR

On the other end, Credit Suisse’s analyst, Richard Hitchens, in a research note last month looked at valuation dispersion, basically volatility of valuation in reference to their average across our local market. He expects to remain low. He goes on to suggest that quality stocks are cheap if quality is defined by companies that are traditionally at higher price earnings ratio.

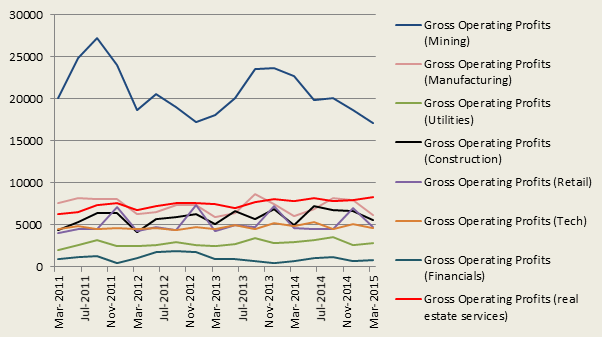

Australian Company Earnings by Sector

Data Source: RBA

Valuation is also about cash flows, growth of those cash flows and inherent riskiness of the cash flows. Australian company earnings are not improving. Earnings of miners are spiralling with only real estate, utilities and financials showing a bit of positivity. However, these three sectors are not going offset the lion’s share of Australia’s economy… mining.

Moreover, the Chinese economy is unwinding and the only reason the financial market isn’t crashing is because it is not a free market anymore. So valuations may be quite low, but we don’t see much growth in those cash flows.

We would encourage investors to not look for value in Australia at this stage. For growth, the U.S. is hard to go past, along with a few emerging markets.

We don’t see a convergence occurring anytime soon.