Source: ProVision

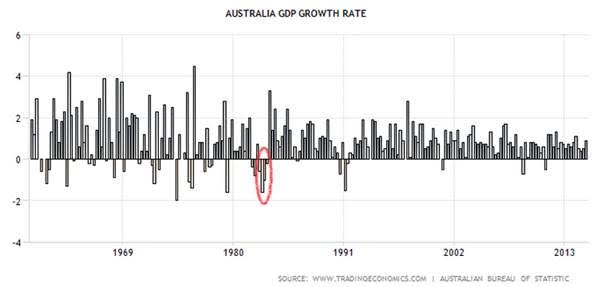

It has now been 7-8 years since the Global Financial Crisis (GFC). With the mining boom over, high unemployment rate at 6.3%, weakening consumer & business confidence and government’s further cutting R&D, there is a likelihood of Australia entering recession for the first time since the early 1990s. The chart below shows in red that Australia’s last recession came right after Black Monday of October 1987.

Source: www.tradingeconomics.com

Many analysts are drawing comparisons between the recent Chinese market crash and Black Mondayin the U.S. on October 1987, where the market fell nearly 30% in a single trading session.

How should investors position themselves for a possible recession?

Could this be a time for an Australian market crash?

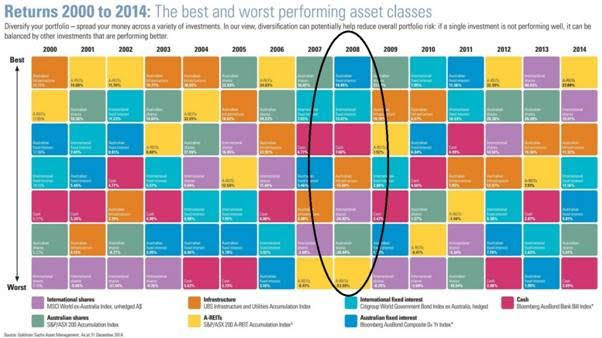

The most stringent stress test for any portfolio is to examine the returns of asset classes during the GFC. The table below illustrates Australian asset class returns, which gives us an indication: be underweight Australian equities and property and overweight Australian and international bonds.

Best and worst performing asset classes: 2000 to 2014

Source: Goldman Sachs

Although property as an asset class is performing extremely well right now, the underweight position at current levels fits nicely with all the recent doom and gloom of an imminent crash in Australia’s property market. This is driven by a concern that Australia’s low interest rate could push property investors and developers into riskier commercial real estate.

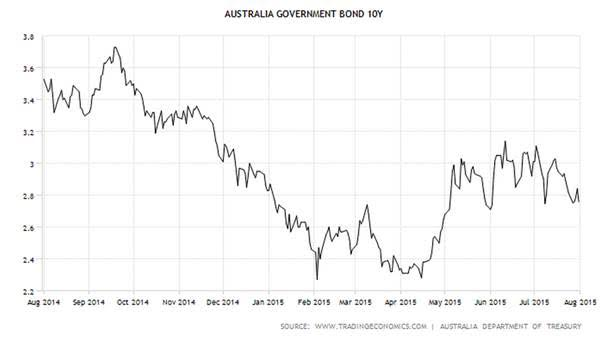

Bond yields are low

Bond yields have been coming back down and consolidating after rising from April to June in the midst of the Greek debacle coming to a close. Low bond yields suggest that investors are more cautious and therefore require a lower yield to buy safe assets such as bonds.

Source: www.tradingeconomics.com

Low bond yields should not deter investors from being in the market, as these investments are for income and protection purposes during a downturn rather than for capital appreciation and growth. They are an ideal asset class for a potential impending correction.

Do not short Australian equities

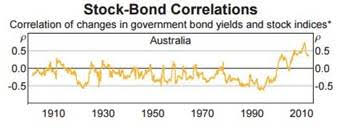

Source: RBA

While we remain selective in our stock selection, being underweight equities does not necessarily imply going short.

Bear in mind that equity prices and bond yields are negatively correlated for the most part. However, they may turn positive. During the GFC, the correlation between the two reached ~0.5, which implies that a 1% fall in equities, led to a 0.5% fall in bonds, all being equal. So going short equities while being long bonds may turn out to be a double exposure to a downturn. That is not a well-balanced portfolio. In the event of a continuing bull market, investors will achieve lower returns.

Conclusion

It is important for Investors to look at history, to give themselves a guide on how to position their portfolios. The prescription right now is straightforward.

Be aware of Australian equities, don’t chase rising property prices and focus on bonds that give high yields. All the while, keeping the portfolio well-diversified and cushioned against an upcoming recession.